2025 TAX BRACKETS

Notable changes for tax year 2025

The tax year 2025 adjustments described below generally apply to income tax returns to be filed starting tax season 2026. The tax items for tax year 2025 of greatest interest to many taxpayers include the following:

For tax year 2025, the standard deduction amounts:

$15,750 for Single filers and Married Filing Separately

$23,625 for Heads of Households

$31,500 for Married Filing Jointly and Qualifying Surviving Spouses

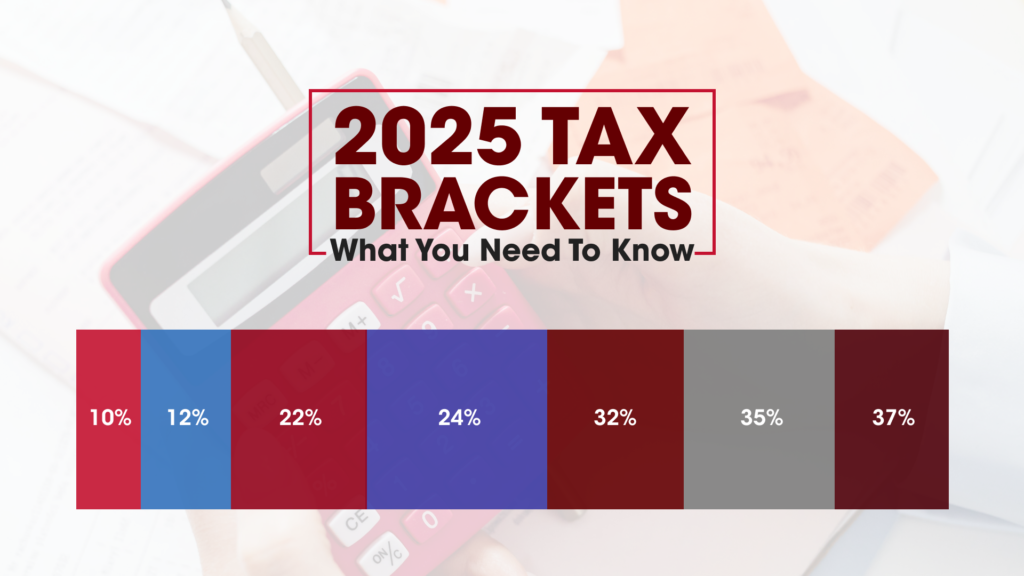

TAX BRACKETS FOR YEAR 2025

Marginal rates. For tax year 2025, the top tax rate remains 37% for individual single taxpayers with incomes greater than $626,350 ($751,600 for married couples filing jointly). The other rates are:

35% for incomes over $250,525 ($501,050 for married couples filing jointly).

32% for incomes over $197,300 ($394,600 for married couples filing jointly).

24% for incomes over $103,350 ($206,700 for married couples filing jointly).

22% for incomes over $48,475 ($96,950 for married couples filing jointly).

12% for incomes over $11,925 ($23,850 for married couples filing jointly).

10% for incomes $11,925 or less ($23,850 or less for married couples filing jointly).

Alternative minimum tax exemption amounts. For tax year 2025, the exemption amount for unmarried individuals increases to $88,100 ($68,650 for married individuals filing separately) and begins to phase out at $626,350. For married couples filing jointly, the exemption amount increases to $137,000 and begins to phase out at $1,252,700.

Earned income tax credits

For qualifying taxpayers who have three or more qualifying children, the tax year 2025 maximum Earned Income Tax Credit amount is $8,046, an increase from $7,830 for tax year 2024. The revenue procedure contains a table providing maximum EITC amount for other categories, income thresholds and phase-outs.

Qualified transportation fringe benefit. For tax year 2025, the monthly limitation for the qualified transportation fringe benefit and the monthly limitation for qualified parking rises to $325, increasing from $315 in tax year 2024.

Health flexible spending cafeteria plans. For the taxable years beginning in 2025, the dollar limitation for employee salary reductions for contributions to health flexible spending arrangements rises to $3,300, increasing from $3,200 in tax year 2024. For cafeteria plans that permit the carryover of unused amounts, the maximum carryover amount rises to $660, increasing from $640 in tax year 2024.

Medical savings accounts. For tax year 2025, participants who have self-only coverage the plan must have an annual deductible that is not less than $2,850 (a $50 increase from the previous tax year), but not more than $4,300 (an increase of $150 from the previous tax year).

The maximum out-of-pocket expense amount rises to $5,700, increasing from $5,550 in tax year 2024.

For family coverage in tax year 2025, the annual deductible is not less than $5,700, increasing from $5,550 in tax year 2024; however, the deductible cannot be more than $8,550, an increase of $200 versus the limit for tax year 2024. For family coverage, the out-of-pocket expense limit is $10,500 for tax year 2025, rising from $10,200 in tax year 2024.

Foreign earned income exclusion. For tax year 2025, the foreign earned income exclusion increases to $130,000, from $126,500 in tax year 2024.

Estate tax credits. Estates of decedents who die during 2025 have a basic exclusion amount of $13,990,000, increased from $13,610,000 for estates of decedents who died in 2024.

Annual exclusion for gifts increases to $19,000 for calendar year 2025, rising from $18,000 for calendar year 2024.

Adoption credits. For tax year 2025, the maximum credit allowed for an adoption of a child with special needs is the amount of qualified adoption expenses up to $17,280, increased from $16,810 for tax year 2024.

Unchanged for tax year 2025

By statute, certain items that were indexed for inflation in the past are currently not adjusted.

Personal exemptions for tax year 2025 remain at 0, as in tax year 2024. The elimination of the personal exemption was a provision in the Tax Cuts and Jobs Act of 2017.

Itemized deductions. There is no limitation on itemized deductions for tax year 2025, as in tax year 2024 and preceding, to tax year 2018. The limitation on itemized deductions was eliminated by the Tax Cuts and Jobs Act of 2017.

Lifetime learning credits. The modified adjusted gross income amount used by taxpayers to determine the reduction in the Lifetime Learning Credit provided in Sec. 25A(d)(1) of the Internal Revenue Code is not adjusted for inflation for taxable years beginning after Dec. 31, 2020. The Lifetime Learning Credit is phased out for taxpayers with modified adjusted gross income in excess of $80,000 ($160,000 for joint returns).

What Is a Tax Bracket?

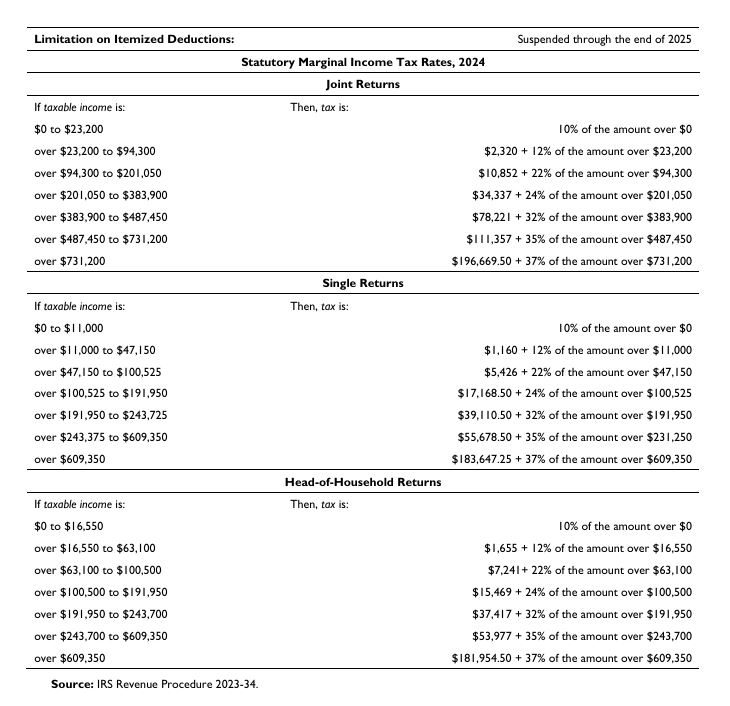

A tax bracket refers to a range of incomes subject to a certain income tax rate. Tax brackets are part of a progressive tax system, in which the level of tax rates progressively increases as an individual’s income grows. Low incomes fall into tax brackets with relatively low income tax rates, while higher earnings fall into brackets with higher rates. The Internal Revenue Service (IRS) Provides "Tax Inflation Adjustments" for each tax year. The Internal Revenue Service (IRS) announces any changes to tax brackets and rates annually. The table above shows the FEDERAL TAX BRACKETS for year 2023 AND 2024.

KEY POINTS RELATED TO THE FEDERAL TAX BRACKETS

- There are currently seven federal tax brackets in the United States, with rates ranging from 10% to 37%.

- The U.S. tax system is progressive, with people in lower brackets taxed at lower rates and those in higher brackets taxed at higher ones.

- Unless your total income fits in just the lowest tax bracket, you are charged at multiple rates, according to the additional brackets into which your income flows.

- You are not simply taxed at the rate of the bracket into which your total income falls; therefore, you effectively pay less than that rate.

- Typically, the IRS adjusts tax brackets for inflation every year.

- Your "ACTUAL" tax bracket is based on your Adjusted Gross Income (AGI). So the lower your Adjusted Gross Income (AGI) is, the less you will be taxed.

- The way to lower your AGI is to have more tax deductions or DEFER some of your income.

Example of FEDERAL Tax Brackets:

Below is an example of marginal tax rates for a single filer based on 2022 tax rates.

- Single filers with less than $10,275 in taxable income are subject to a 10% income tax rate (the lowest bracket).

- Single filers who earn more than $10,275 will have the first $10,275 taxed at 10%, but earnings beyond the first bracket and up to $41,775 will be taxed at a 12% rate (the next bracket).

- Earnings from $41,776 to $89,075 are taxed at 22%, the third bracket.4

Consider the following tax responsibility for a single filer with a taxable income of $50,000 in 2022:

- The first $10,275 is taxed at 10%: $10,275 × 0.10 = $1,027.50

- Then $10,276 to $41,775, or $31,499, is taxed at 12%: $31,499 × 0.12 = $3,779.88

- Finally, the remaining $8,225 (what’s left of the $50,000 income) is taxed at 22%: $8,225 × 0.22 = $1,809.50

Add the taxes owed in each of the brackets:

- Total taxes: $1,027.50 + $3,779.88 + $1,809.50 = $6,616.88

The individual’s effective tax rate is approximately 13% of income:

- Divide total taxes by annual earnings: $6,616.88 ÷ $50,000 = 0.13

- Multiply 0.13 by 100 to convert to a percentage, which is 13%

Pros and Cons of Tax Brackets:

Tax brackets—and the progressive tax system that they create—contrast with a flat tax structure, in which all individuals are taxed at the same rate, regardless of their income levels.

Pros

- Higher-income individuals are more able to pay income taxes and keep a good living standard.

- Low-income individuals pay less, leaving them more to support themselves.

- Tax deductions and credits give high-income individuals tax relief, while rewarding useful behavior, such as donating to charity.

Cons

- Wealthy people end up paying a disproportionate amount of taxes.

- Brackets make the wealthy focus on finding tax loopholes that result in many underpaying their taxes, depriving the government of revenue.

- Progressive taxation leads to reduced personal savings.

The 4 minute 30 second video above by CPA Brian Kim, explains the Tax Brackets in a basic way for beginners. Brian is a long time mentor of ours. He has many spot on videos so look up his channel.

WHO WANTS TO PUT MORE MONEY IN YOUR POCKET?

WHY GIVE IT AWAY TO THE IRS?

Above is a detailed video (less than 9 minutes) explaining the tax brackets in greater detail. It gives great explanations and ideas on how to reduce your taxable income which is your AGI (Adjusted Gross Income). As we discussed, by simply lowering your taxable income, you may qualify for even more tax credits and further reduce your tax liabilities which ultimately puts more money in your pocket annually and may contribute to more money available to you at the time of your desired retirement age.

0:00 Intro

0:24 2024 Tax Brackets

1:55 2024 Standard Deductions

2:34 Simple Tax Calculator

4:18 Roth Vs. Traditional Retirement plan tax example

4:45 2024 Retirement Plan Limits

5:44 Tax Credit and Deductions

7:09 Retire Early

State Tax Brackets

Some states have NO INCOME TAX:

1. Alaska,

2. Florida,

3. Nevada,

4. South Dakota,

5. Tennessee,

6. Texas,

7. Washington, and

8. Wyoming.

9. New Hampshire doesn’t tax earned wages, but it does tax investment income and interest. However, it is set to phase out those taxes starting in 2023, bringing the number of states with no income tax to nine by 2027.

In 2022, nine states had a flat rate structure, with a single rate applying to a resident’s income:

- Colorado (4.55%),

- Illinois (4.95%),

- Indiana (3.23%),

- Kentucky (5.0%),

- Massachusetts (5.0%),

- Michigan (4.25%),

- North Carolina (5.25%),

- Pennsylvania (3.07%), and

- Utah (4.95%).

In other states, the number of tax brackets varies from three to as many as nine (in California, Iowa, and Missouri) and even 12 (in Hawaii). The marginal tax rates in these brackets also vary considerably. California has the highest, maxing out at 12.3%.

State income tax regulations may or may not mirror federal rules. For example, some states allow residents to use the federal personal exemption and standard deduction amounts for figuring state income tax. In contrast, others have their own exemption and standard deduction amounts.