IF YOU HAVE RECEIVED A NOTICE FROM THE IRS OR FROM YOUR STATE TAXATION DEPARTMENT; YOU CAN UPLOAD THE NOTICE AT THE LINK BELOW.

IF YOU WOULD LIKE TO HAVE A PERSONALIZED LETTER FROM US TO SEND IN TO THE IRS OR TO YOUR STATE TAX DEPARTMENT; WE WILL DRAFT ONE FOR A PREPAID FEE OF $75 PER LETTER.

BE ADVISED, WE DO NOT MAIL ANY NOTICES TO THE IRS NOR TO ANY STATE TAXATION DEPARTMENT ON YOUR BEHALF. THAT IS YOUR RESPONSIBILITY TO REPLY AND SEND THEM WHAT THEY ARE ASKING FOR ON THE NOTICE.

AVOID TAX PENALTIES IN 2025

KNOW YOUR RELIEF OPTIONS

Tax penalties can quickly turn an already stressful situation into a financial nightmare. Whether due to late filing, underpayment, or incorrect information, penalties imposed by the IRS can add up fast, making tax debt even more difficult to manage. However, many taxpayers don’t realize that there are ways to reduce or even eliminate these penalties

WATCH THE VIDEO PRESENTATION BELOW TO LEARN MORE

INTRODUCTION TO FILING AN APPEAL WITH

YOUR STATE TAXATION AGENCY

One frequent question that arises is the extent to which U.S. income tax treaties can apply to reduce state income tax.

The prevailing opinion is that income tax treaties are limited to “federal income taxes imposed by the Internal Revenue Code” as stated in the treaty, but that opinion is incorrect.

This incorrectness is especially true regarding States that Defer to Section 61.

Regarding States that Defer to Section 61; which most states (but not all) do in fact defer to Internal Revenue Code section (herein “Section”) 61 for the definition of “gross income.”[1] Section 61 states “Except as otherwise provided in this subtitle, gross income means all income from whatever source derived.” The key phrase here is “[e]except as otherwise provided in this subtitle.”

This phrase means that other provisions in Title 26, Subtitle A, of the U.S. Code modify Section 61. One such provision under Subtitle A is Section 894

Section 894(a)(1) mandates that all “provisions of [the Internal Revenue Code] shall be applied to any taxpayer with due regard to any treaty obligation of the United States which applies to such taxpayer.”

In other words, Section 61 is statutorily modified and to be applied consistent with any treaty obligation that applies to a taxpayer.[2] By operation of Section 894(a)(1), Section 61 is modified to the extent there is an applicable income tax treaty.

Therefore, if the state defers to Section 61 for the definition of gross income, which is modified by any applicable income tax treaty in accordance with Section 894(a)(1), then it logically follows that any income excluded from an individual U.S. federal income tax return pursuant to an applicable income tax treaty is excludible on said individual’s state individual income tax return.

States that Do Not Defer to Section 61, Where federal and state statutes and regulations are substantially identical, the interpretation and effect given to the statute by federal courts is highly persuasive. [3] That being said, even in states where state tax law does not expressly defer to Section 61 yet defines gross income in a substantially identical manner, there is legal authority for the proposition that income tax treaties apply.

There are more specifics to the IRS tax Codes, Case law and other relevant details that we will reference which are not listed here on this page. Those details will be added to and addressed in any letter that we draft on your behalf.

KNOW YOUR RIGHTS AND HOW

TO FILE A RESPONSE TO ANY DENIAL NOTICE, ADJUSTMENT NOTICE OR A REQUEST FOR REPAYMENT NOTICE;

WITH ADDED FEE'S, PENALTIES AND INTEREST.

* WATCH THIS 2 PART WEBINAR *

Notices & Denials Webinar Part 1

Notices & Denials Webinar Part 2

IRS (FEDERAL) AND STATE NOTICES AND DENIALS

* ARE YOU IN A STATE THAT IS DENYING YOUR INCOME TAX EXEMPTION TREATY?

* ARE YOU READY TO KNOW YOUR RIGHTS AND TAKE A POSITION TO APPEAL IF YOUR STATE DENYS THE INCOME TAX TREATY?

* WHAT IF YOUR STATE AND RECALCULATES YOUR TAX RETURN WHICH RESULTS IN YOU GETTING A REDUCED REFUND?

* WHAT IF YOUR STATE CAUSED YOU TO OWE TAXES BY NOT HONORING THE TAX TREATY; NO FAULT OF YOUR OWN?

* DO YOU KNOW WHICH STATES CLEARLY STATE AND POST THAT THEY DO NOT HONOR FEDERAL TAX TREATIES?

GENERALLY, IF THE TAX TREATY DOES NOT COVER A PARTICULAR KIND OF INCOME, OR IF THERE IS NOT A SPECIFIC TREATY BETWEEN YOUR COUNTRY AND THE STATE YOU RESIDE IN, THEN YOU MUST PAY TAX ON THE INCOME IN THE SAME WAY AND AT THE SAME RATES SHOWN IN THE INSTRUCTIONS FOR THE APPLICABLE U.S. TAX RETURN.

MANY OF THE INDIVIDUAL STATES OF THE UNITED STATES TAX INCOME WHICH IS SOURCED IN THEIR STATE. THEREFORE, YOU SHOULD CONSULT THE TAX AUTHORITIES OF THE STATE FROM WHICH YOU DERIVE INCOME TO FIND OUT WHETHER ANY STATE TAX APPLIES TO ANY OF YOUR INCOME.

IT IS WELL KNOWN, THAT SOME STATES OF THE UNITED STATES DO NOT HONOR THE PROVISIONS OF FEDERAL TAX TREATIES.

BELOW IS A PICTURE TAKEN FROM THE IRS WEBSITE WHICH SHOWS WHO IS ON FILE WITH THE IRS DISCLOSING THAT THEY DO NOT HONOR FEDERAL TAX TREATIES.

DO STATES CONFORM TO THE FEDERAL TAX TREATIES?

The States are not bound to honor Federal tax treaties, but most do.

State income tax forms usually start with federal taxable income, or federal adjusted gross income, and require a few adjustments. Income excluded by US treaties are usually excluded from States income tax.

However, several States "DO NOT HONOR" Federal Tax treaties: if you live or work in one of these states, you will most likely owe State income tax even though your income is exempt from Federal income tax by a treaty.

Those are:

- Alabama

- Arkansas

- Connecticut

- Hawaii

- Kansas

- Kentucky

- Maryland

- Mississippi

- Montana

- New Jersey

- North Dakota

- Pennsylvania

- Occasionally in specific situations - California. (It may be excluded for California Tax only if the treaty specifically excludes the income for state purposes. If the treaty does not, California requires the reporting of adjusted gross income from all sources.)

The states that do not impose an income tax on individuals are:

- Alaska

- Florida

- Nevada

- South Dakota

- Texas

- Washington

- and Wyoming

States that do not impose an income tax on wages are:

- New Hampshire

- and Tennessee

Many states use federal taxable income as the starting point for determining state income tax liability.

As a result, if there is no federal taxable income there may also not be any state taxable income.

However, a number of states define federal taxable income by reference only to the U.S. federal income tax rules without regard to treaty rules and require an “add-back” to federal taxable income for any income that is excluded under a treaty.

Audits and Adjustments

Hawaii 2025

Income Tax Explained

(4 Part Webinar)

Hawaii 2025 Webinar Part 1

Hawaii 2025 Webinar Part 2

Hawaii 2025 Webinar Part 3

Hawaii 2025 Webinar Part 4

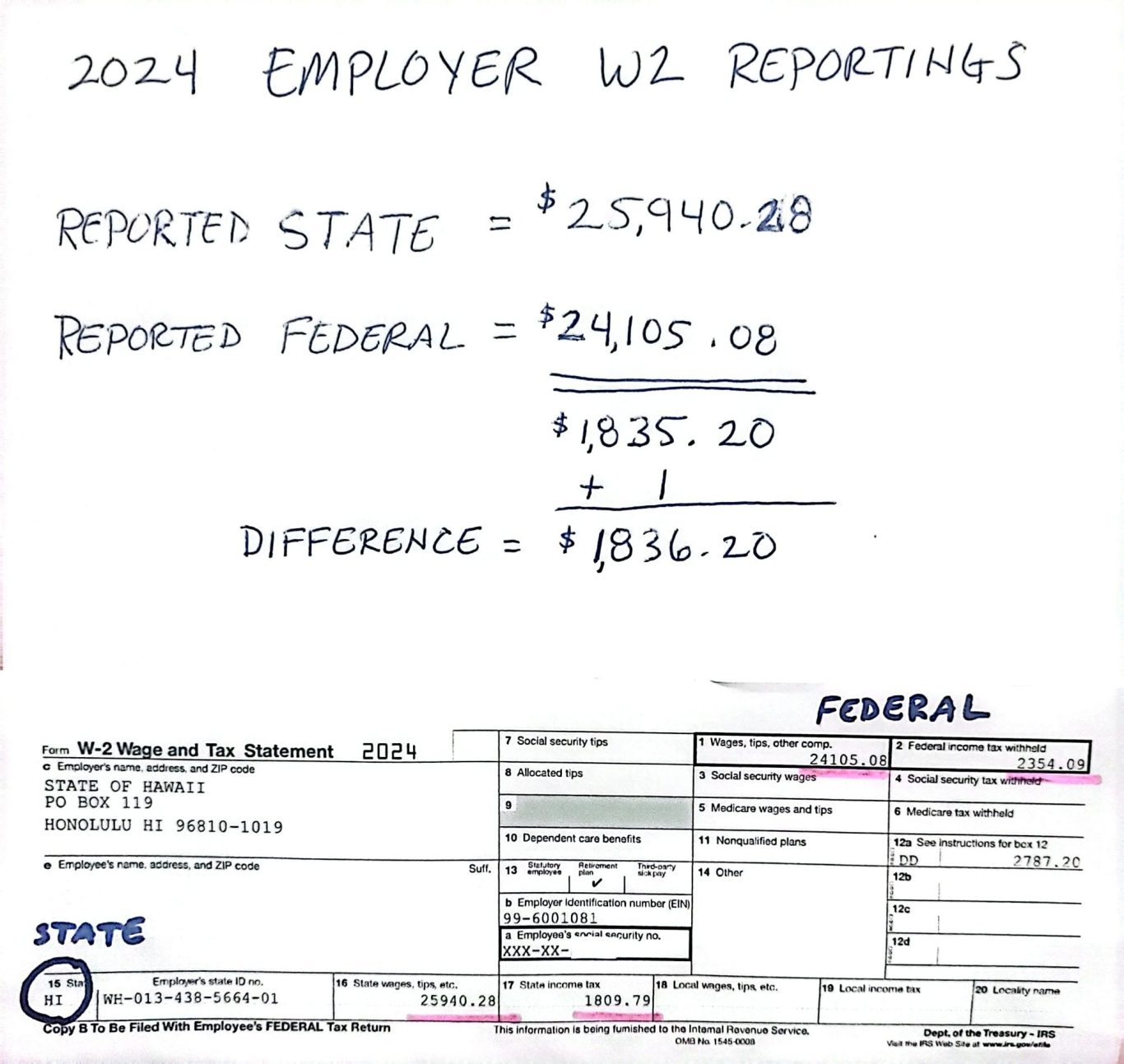

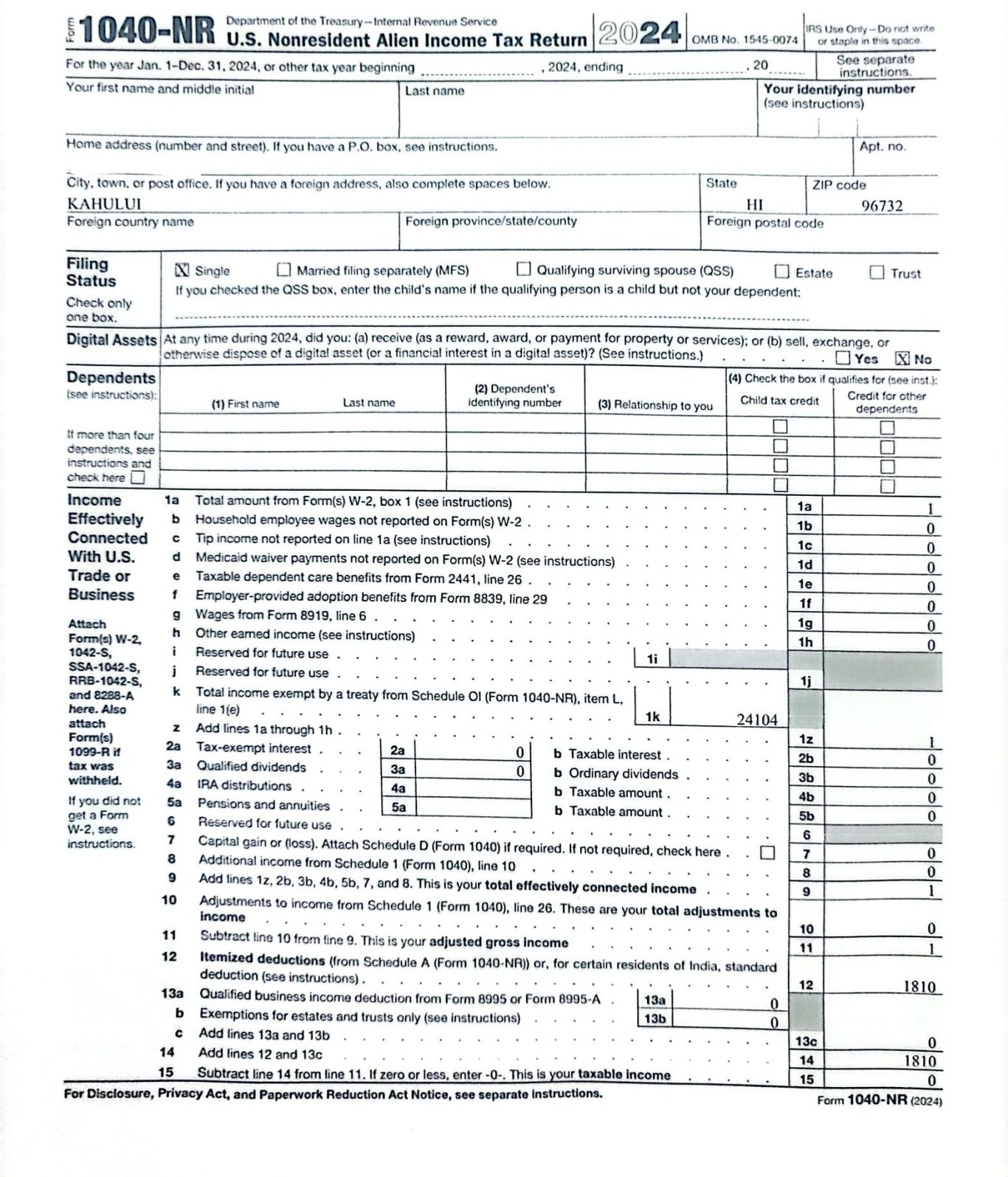

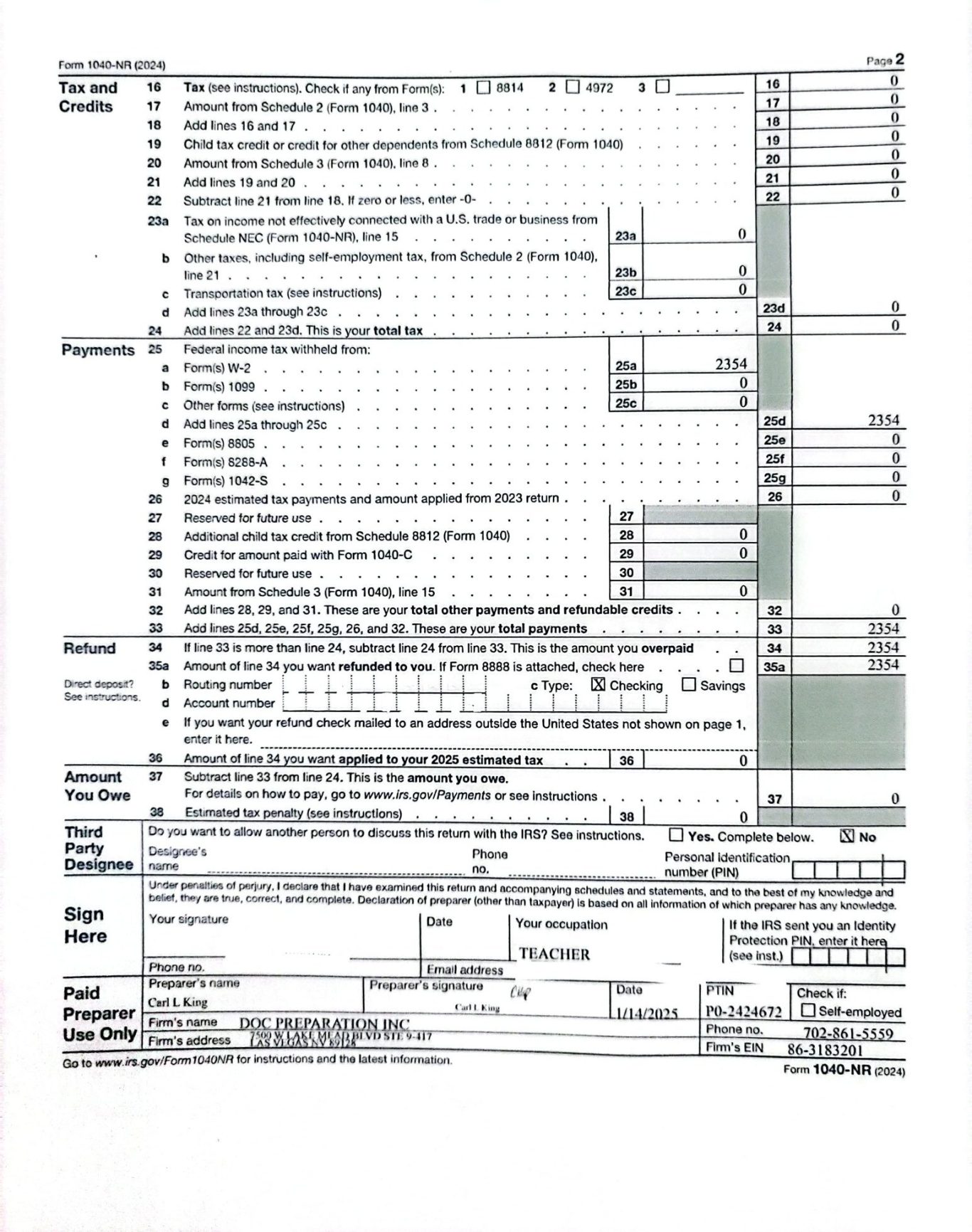

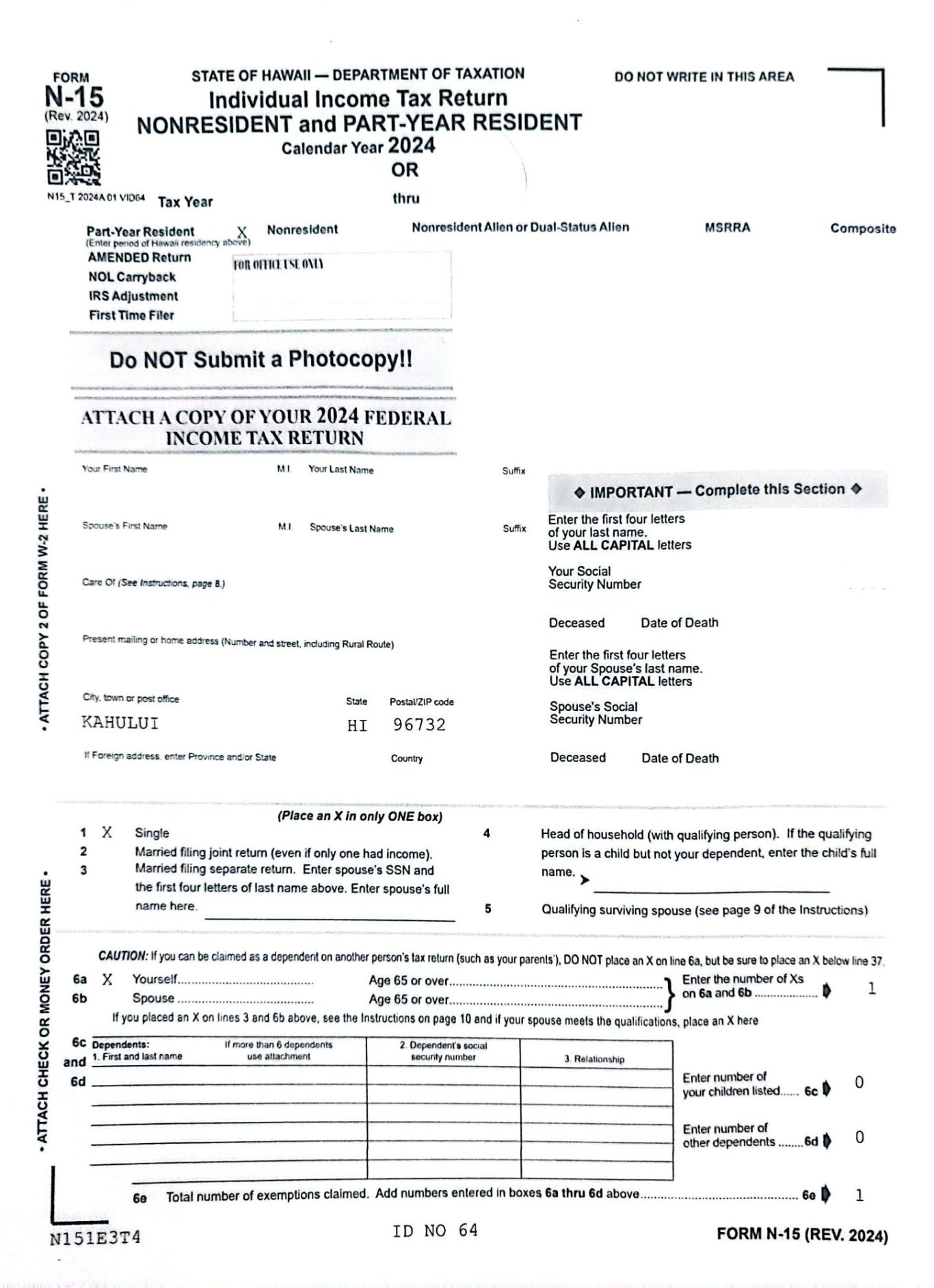

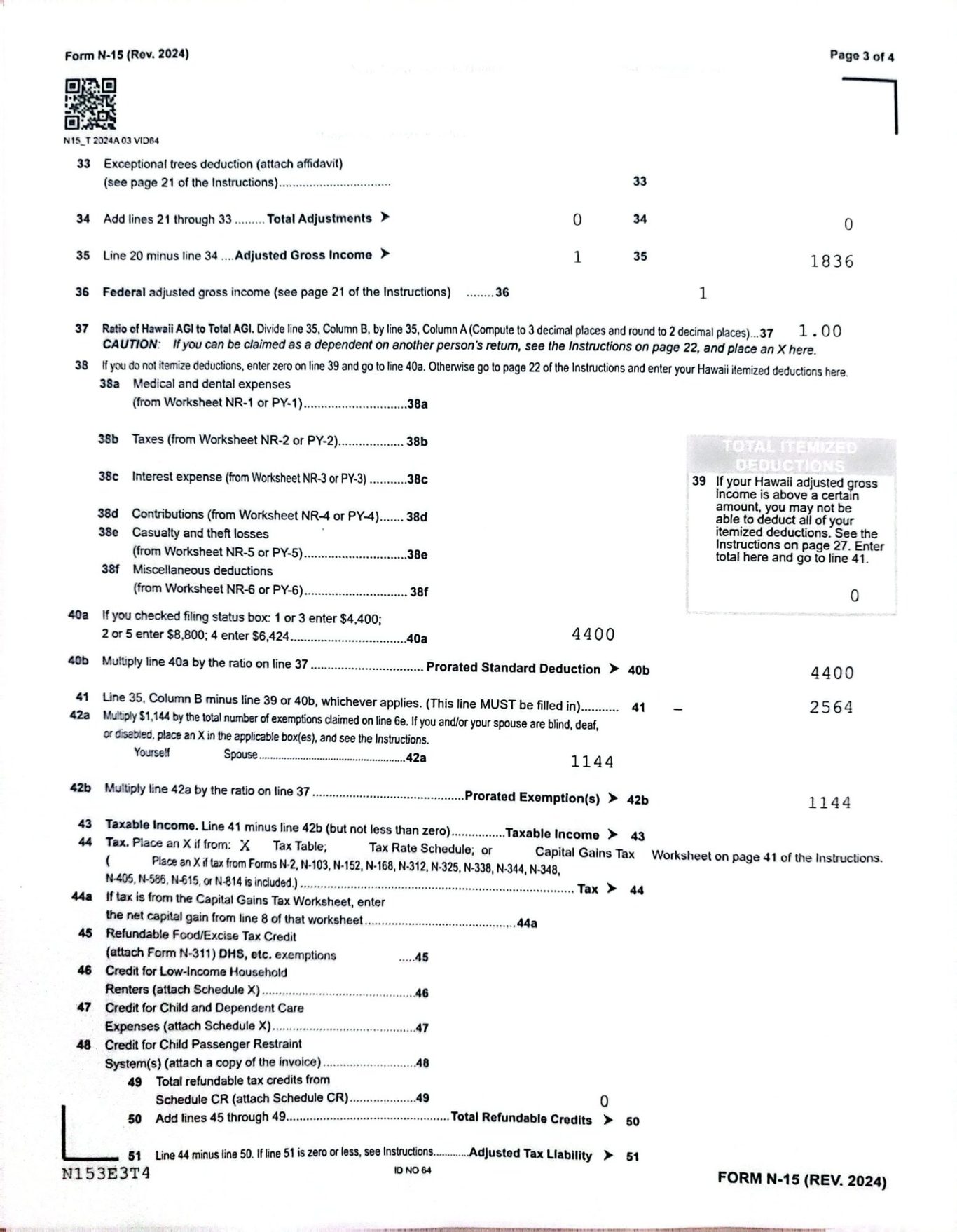

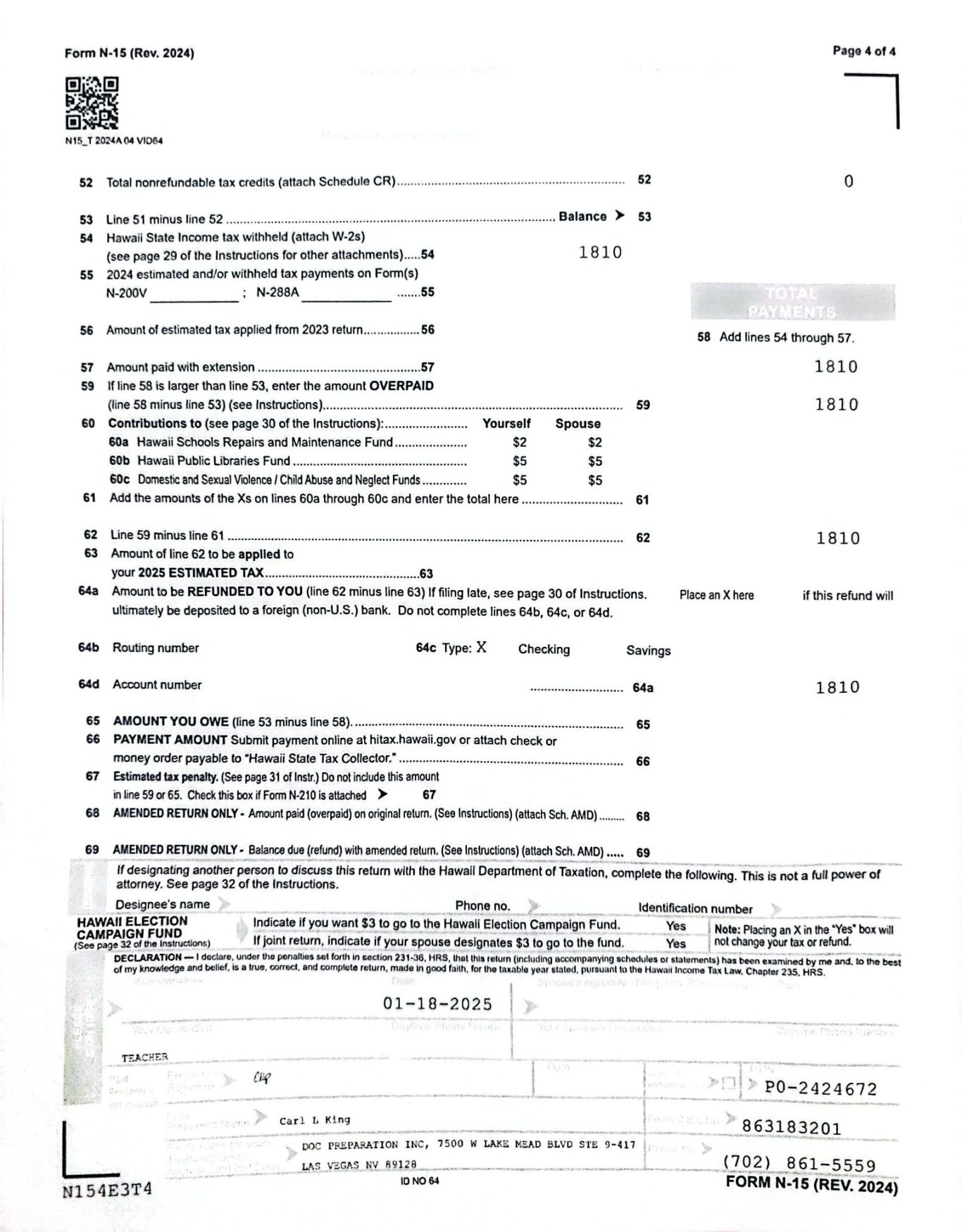

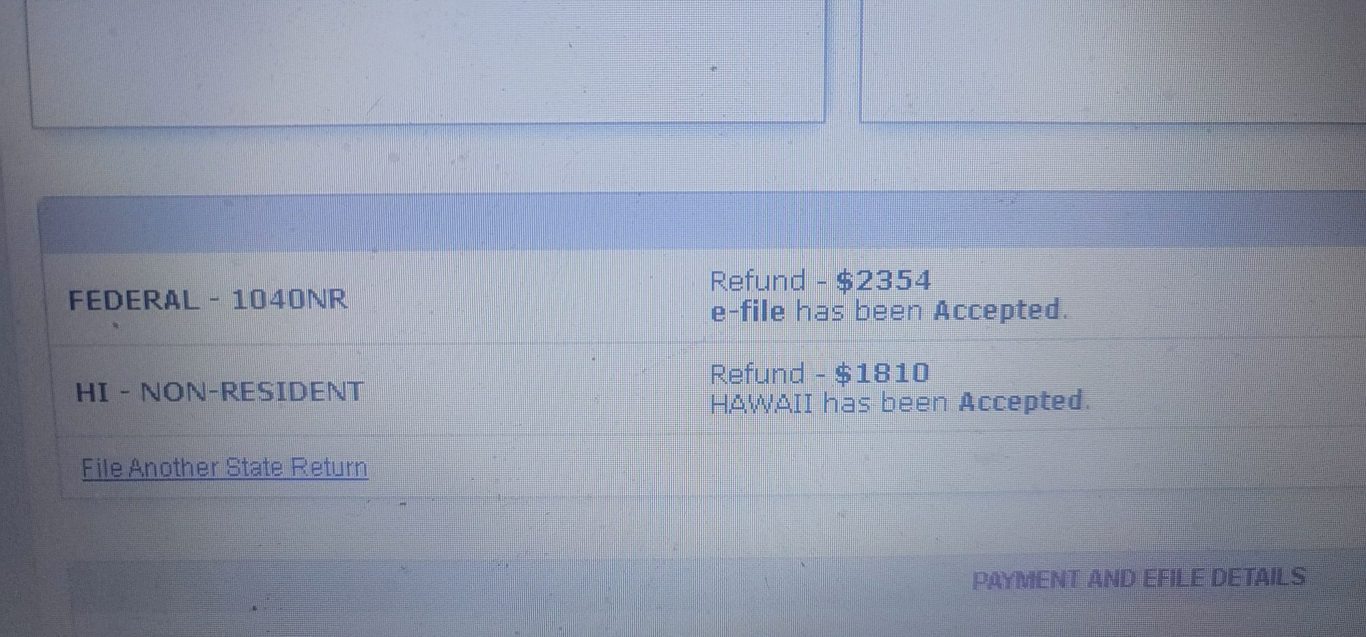

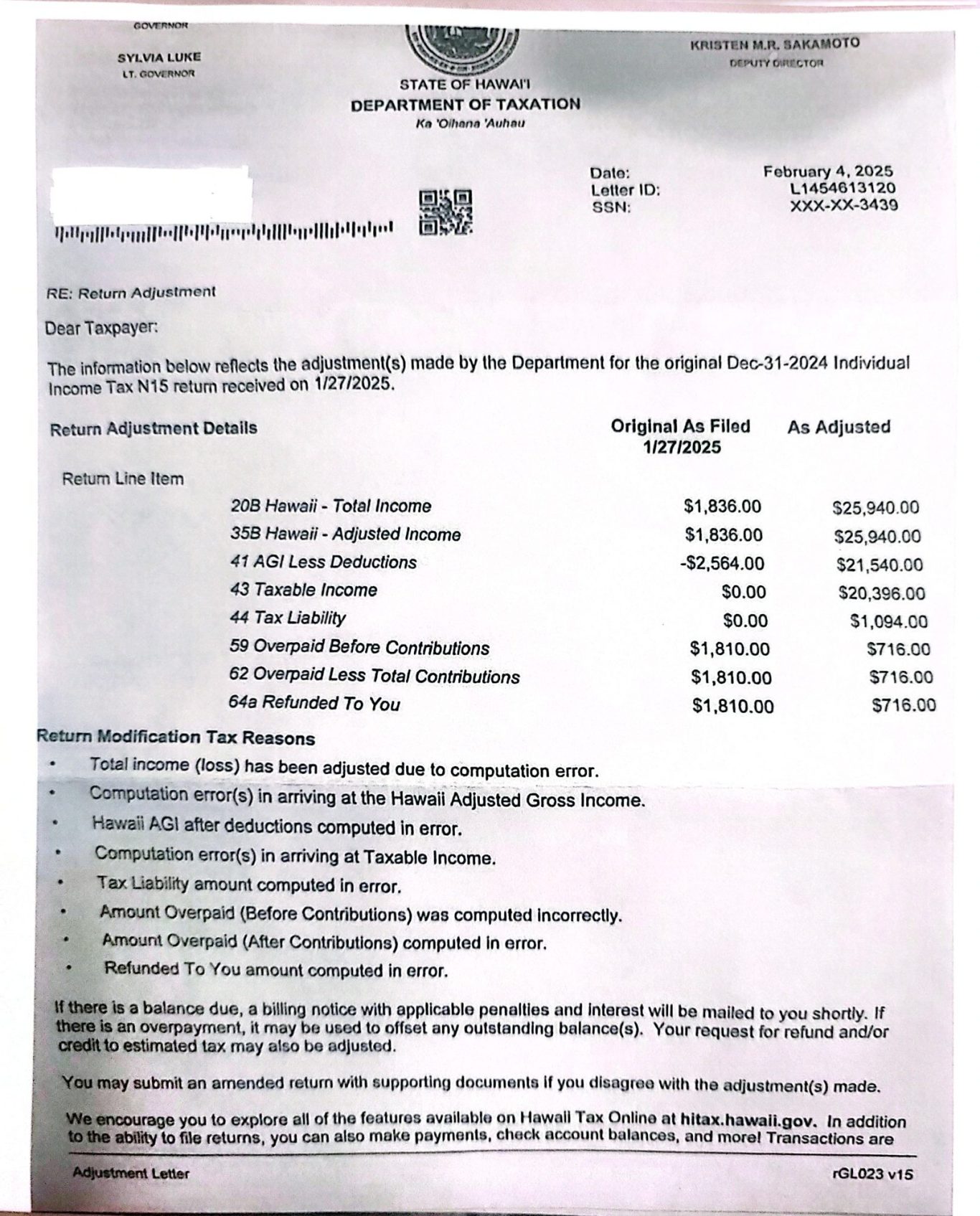

EXAMPLE:

STATE OF HAWAII TAX AUDIT

DENYING A J1 TEACHER THE TAX TREATY EXEMPTIONS

THIS HAWAII CLIENT'S FEDERAL AND STATE TAX RETURNS WERE

PROPERLY PREPARED.

ALL CALCULATIONS ARE 100% ACCURATE BASED ON SUBMITTING THE INCOME TAX TREATY BASED EXEMPTIONS.

BOTH FEDERAL AND STATE TAX RETURNS WERE EFILED

AND ACCEPTED.

SUMMARY:

THE STATE OF HAWAII HAS SENT THIS TAXPAYER CLIENT AN ADJUSTMENT NOTICE CLAIMING THAT THE FIGURES ARE WRONG.

THIS IS NOT TRUE. THE RETURN WAS PROPERLY PREPARED

AND NO ERRORS WERE MADE.

THE STATE OF HAWAII IS SIMPLY ELECTING TO NOT HONOR THE TAX TREATY WHICH HAS EXEMPTED THE TAXPAYERS TAX LIABILITY.

THE STATE OF HAWAII HAS MADE ADJUSTMENTS TO THE ORIGINAL TAX RETURN FILED. THESE AJDUSTMENTS SHOW THAT THE TAXPAER HAS A TAX LIABILITY AND HAS REDUCED THE TAXPAYERS REFUND ACCORDINGLY.

OUR TAX PREPARES HAVE NO CONTROL IF THE IRS OR STATE TAX AGENCY ELECTS TO MAKE ANY ADJUSTMENTS TO YOUR RETURN.

WE AS A COMPANY, MYSELF AS AN ERO, NOR ANY OF OUR TAX PREPARERS ARE OBLIGED TO REPRESENT YOU IN THESE MATTERS BEFORE THE IRS OR ANY STATE TAXATION AGENCY.

WE ARE NOT OBLIGED FILE AMENDMENTS OR CONTACT THE

IRS/STATE TAXATION AGENCIES ON YOUR BEHALF.

OUR SERVICES FOR DOCUMENT PREPARATION OF YOUR TAX FORMS

WERE COMPLETE WHEN YOU RECIEVED YOUR TAX RETURN FILE.

YOU CAN ELECT TO RETAIN OUR FIRM OR REQUEST ADDITIONAL SERVICE FOR A FEE.

Requesting an Abatement in Hawaii

Now lets Talks about State Tax issues similar to Federal taxes.

Each State has their own forms and guidelines to follow when requesting an abatement regarding State imposed penalties, fees and interrest.

The Example used here today pertains to the State of Hawaii Departmewnt of Taxation.

The State of Hawaii has what's called a "Offer in Compromise"

By law, taxes should be paid in full and on time.

When that is not possible, other options may be available. For example, a payment plan in which the amount due (plus any penalty and interest that is charged after the filing deadline) is paid in monthly installments with interest accruing monthly on the unpaid tax and penalty amount.If a payment plan will not work, you may ask the Department of Taxation (Department) to compromise on the amount of the tax, penalty, and interest due.

This request to pay less than what is actually owed to settle a taxpayer’s delinquency is known as an offer in compromise.

The following answers some of the most commonly asked questions about offers in compromise.

1) What is an offer in compromise?

An offer in compromise is a request by you to the Department to pay less than the total amount of delinquent tax, penalty, and interest actually owed to the state.

2) When is an offer in compromise appropriate?

An offer in compromise may be appropriate when there is doubt as to the amount of the tax liability, doubt as to the collectability of the tax liability, or exceptional circumstances (effective tax administration).

3) What is doubt as to liability?

Doubt as to liability means that there is some uncertainty about whether the amount that the Department says is owed is in fact the correct amount.

Possible reasons for submitting a doubt as to liability offer in compromise include the following: the examiner made a mistake interpreting the tax law, the examiner failed to consider the evidence presented, or new evidence is available to support a change to the assessment.

Caution: You may not ignore audit notifications sent by the Department and later attempt to make an offer in compromise based on doubt as to liability based on records that were available to you at the time of the audit but chose not to produce. An offer in compromise is not a substitute for appearing at an examination and producing records to support your position.

4) What is doubt as to collectability?

Doubt as to collectability means that the Department does not think that you will ever be able to pay the full amount of the taxes, penalties, and interest owed no matter how long the Department waits. For example, there may be doubt as to collectability when you have an outstanding tax liability and no assets, are in poor health (which is substantiated with a physician’s report), and have no future earning potential.

5) What is exceptional circumstances (effective tax administration)?

Exceptional circumstances (effective tax administration) means that although you have sufficient assets to pay the full amount of tax owed, due to exceptional circumstances, requiring full payment would cause an economic hardship or would be unfair and inequitable. For example, you may have a serious illness such that paying the full amount of tax owed would impair your ability to provide for yourself and your family.

6) Should I attach an offer in compromise to my tax return if I cannot pay the full amount of tax shown on the return?

No. File the tax return and wait until you receive a bill from the Department. That will allow the Department to process your return and determine the actual amount of your tax delinquency.

After you receive the bill, contact the Department at the telephone number listed on the bill. Our collection staff will first try to determine if a payment plan is a valid option. If not, then an offer in compromise may be appropriate.

Note: If you are being represented by a tax professional, you must complete a power of attorney (Form N-848) authorizing the Department to discuss your situation with that person. Form N-848 may be obtained from any district tax office, by calling the Department at 808-587-4242 (toll-free at 1-800-222-3229), or on the Department’s website.

7) How do I submit an offer in compromise?

All applications require documentation which will be reviewed and verified.

Complete and send the following:

Form CM-1 Offer in Compromise on website at Hawaii Tax Forms (Alphabetical Listing)

Form CM-2 (Individual) or CM-2B (Corporation) Statement of Financial Condition (Federal Forms are acceptable) on website at Hawaii Tax Forms (Alphabetical Listing)

Copies of all bank statements & bank checks/check register for last 3 months

If applicable, also provide:

___ Copies of statements showing the premium amounts for all insurance (auto, home, health, renters, etc.) – the coverage page of the homeowners & renters insurance policies and the first page of all insurance policies

___ Copies of Federal income tax returns for the last 3 tax years

___ Copies of any and all contracts and notes receivables

___ Copies of any and all judgments, including divorces

___ Real property: Complete name and address of encumbrance/lien holder & proof of remaining balance. Copies of any and all deeds to real property in which you have an interest. Realtor’s valuation, and a copy of the current year’s county assessor’s valuation. If renting, provide a copy of your rent/lease agreement.

___ Vehicles: Copies of all registration certificate(s) issued by the Department of Licensing, verification of any encumbrances against all vehicles plus the current statements. Provide verification of how the values were determined, this includes cars, boats, trucks, motor homes airplanes, etc.)

___ Copies of any and all pre or ante nuptial agreement, with affidavits from each of the parties under penalty of perjury regarding adherence to said agreements

___ Copies of any and all trusts of which you may be a beneficiary or which you have an interest

___ Copies of paychecks/stubs/statements for the last 6 months

___ Proof of all court ordered payments you are making (child/spousal support, fines, etc.)

___ Proof of monthly expenses not already covered, i.e. utility bills, transportation, etc.

___ Doctor’s papers, if claiming ill health or disabled

___ The Source of funds for offer

___ Copy of Federal Offer in Compromise and letter of acceptance

For faster processing, send your pdf documents via web message on Hawaii Tax Online (HTO).

To set-up an account on HTO, visit Hawaii Tax Online at https://hitax.hawaii.gov, or send all applicable forms and documents to:

By mail:

Department of Taxation – Collections Branch

P.O. Box 259

Honolulu, HI 96809-0259

By Fax:

(808) 587-1720

8) Can I use federal Form 656, Offer in Compromise, to submit an offer in compromise to the state?

No. Federal Form 656 cannot be substituted for the Department’s Form CM-1. However, copies of documents that you submit to the Internal Revenue Service (IRS), such as your current financial statements, may be submitted to the Department.

9) Will the Department continue its collection activities after an offer in compromise is submitted?

No. Collection activities (for example, additional liens, levies, garnishments, or referrals to outside collection agencies) against you with regards to the specific tax relating to the offer in compromise are suspended while your offer is being investigated and evaluated. Other types of taxes with collections activities not related to the offer in compromise will continue as normal.

Note: Internal offsets of tax credits are not considered collection activities and therefore, are not suspended while your offer is being evaluated.

If the Department finds that your offer in compromise is a tactic to delay collection actions or if the delay jeopardizes the Department’s ability to collect the outstanding tax liabilities, the Department will take action to protect the state’s interests.

10) I am currently on a payment plan. Do I need to continue making my monthly payments after submitting an offer in compromise?

Yes. You must continue making your monthly installment payments per your installment agreement while your offer in compromise is being considered.

11) How much should I offer for the compromise?

The amount that the Department will accept for an offer in compromise will vary depending on the reason for the compromise. If the compromise is offered because there is doubt as to liability, then the amount offered may be the amount that you believe is the correct tax liability owed. If the compromise is offered because there is doubt as to collectability, then the amount offered is usually the amount that you believe is appropriate given your current financial condition and future earning potential.

12) Is any part of the amount offered in the compromise required to be paid when Form CM-1 is submitted?

Yes. All offers in compromise must be accompanied by a minimum payment. For a lump sum offer in compromise, at least 20% of the proposed offer must accompany the offer. For an offer in compromise that will be paid in periodic installments, an amount equal to the first periodic payment must accompany the offer.

However, the Department may waive these payment requirements for individuals who meet the low income certification guidelines published by the IRS. If the offer in compromise is rejected, any payment made with the offer in compromise will be kept by the Department and will be applied to your tax debt. Payments are applied first to recover costs incurred by the Department, then to any interest due, then to penalties, and finally, to taxes.

For more information, TAX FACTS "Offer in Compromise" you can do some related searches on the Hawaii Dept. of Taxation website. Some things to search are:

- Tax Collections Service

- Make Payment

- Payment Plans

- Wage Levy for Individuals

- Mandatory Electronic Payment (EFT)

- Tax Clearance Certificates

- Information and Options to Resolve Your State Tax Debt